However, retirement planning is essential, and for those who are self-employed, freelancers, and small business owners, the process may be a little more complicated. But understanding the proper retirement plan for your financial objectives is essential. Two of the most popular retirement plans are the Solo 401(k) and the SEP IRA, both of which offer tax benefits but differ in their characteristics and advantages. At Opulent Gold Group, we are committed to assisting you in making the proper financial choices that will ensure your future. In this article, we will discuss the main differences between the Solo 401(k) and SEP IRA, their contribution limits, and how each works. By the end of this article, you will be able to determine which one is best for your financial needs.

Key Differences Between the Solo 401(k) and the SEP IRA

When it comes to retirement planning, the Solo 401(k) and the SEP IRA are two distinct plans that offer distinct benefits to self-employed individuals. It is important to note that there are some main differences between the Solo 401(k) plan and the SEP IRA.

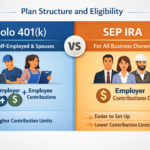

Plan Structure and Eligibility

- Solo 401(k): This type of plan is tailored for self-employed individuals or business owners who do not have any employees, except for their spouse. With the Solo 401(k), you can contribute to your retirement plan as both the employer and the employee, which is quite flexible. If you are a sole proprietor or a small business owner with your spouse as your business partner, then the Solo 401(k) is the best plan for you.

- SEP IRA: In contrast, the SEP IRA is open to all business owners, including sole proprietors, partnerships, and corporations. However, the SEP IRA plan permits contributions only from the employer, not from the employee. It is simpler to set up than a Solo 401(k), but it has lower contribution limits.

Contribution Limits and Flexibility

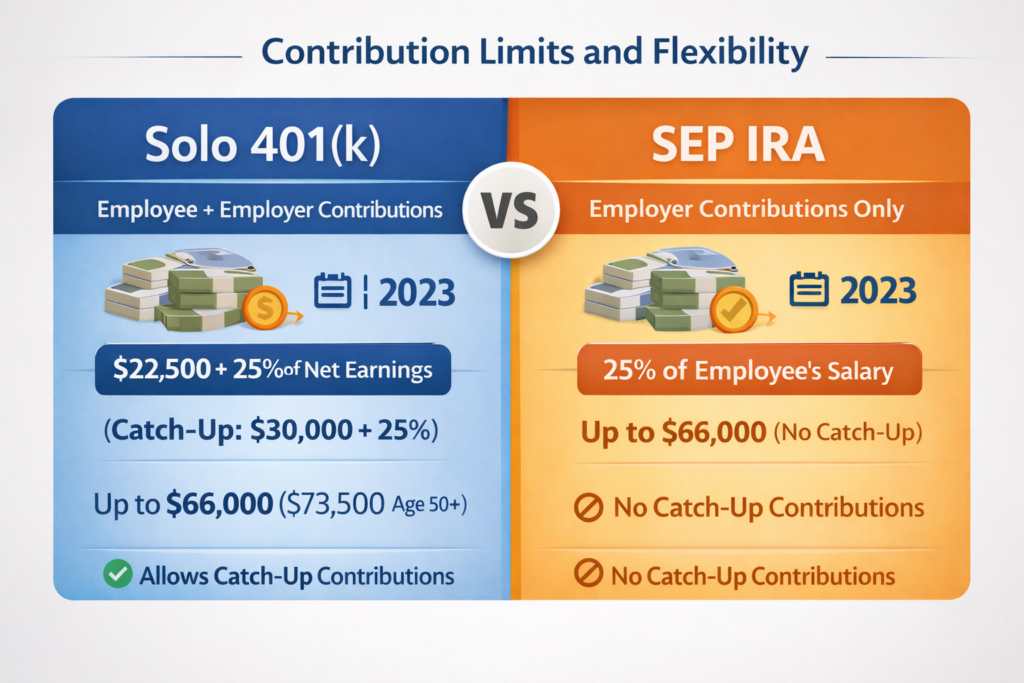

- Solo 401(k): The Solo 401(k) plan has high contribution limits. You can contribute as an employee and as an employer, which means you can contribute more. For 2023, you can defer as much as $22,500 of your income (or $30,000 if you are 50 or older). Moreover, you can also contribute as much as 25% of your net earnings as an employer. This means you can contribute up to $66,000 (or $73,500 if you are 50 or older).

- SEP IRA: The SEP IRA contribution plan is more straightforward. You can contribute up to 25% of the employee’s salary, with a maximum contribution of $66,000 for 2023. The SEP IRA contribution plan does not allow catch-up contributions for individuals who are 50 or older. Only the employer can contribute to the SEP IRA.

Administrative Requirements

- Solo 401(k): Although the Solo 401(k) plan provides great flexibility in terms of contributions, it is not entirely free of administrative complexities. You will be required to file Form 5500 if your account balance exceeds $250,000 at any point during the year. Moreover, there are more administrative tasks involved in the initial setup process, making it a slightly more complicated option to administer.

- SEP IRA: The SEP IRA plan is relatively easy to administer. There are no administrative requirements to be fulfilled when filing with the IRS. This makes it a more convenient option for business owners who want a hassle-free retirement plan. However, this ease of administration comes with drawbacks in terms of flexibility and contribution limits.

The above-mentioned administrative differences between the Solo 401(k) and SEP IRA plans should help you make a more informed decision about which plan is best suited to your business needs and preferences. In the next section, we will examine the contribution levels for both plans to help you make an even more informed decision.

Contribution Rates: Solo 401(k) vs. SEP IRA

One of the most crucial factors to consider when choosing between a Solo 401(k) and a SEP IRA is each plan’s contribution limit. Both plans offer significant tax benefits, but their contribution rates are as different as chalk and cheese.

Breakdown of Contribution Limits for Solo 401(k)

- Employee Contributions: As a business owner, you can contribute as an employee up to 100% of your income, subject to a maximum of $22,500 for 2023 (or $30,000 if you are 50 or older, including catch-up contributions).

- Employer Contributions: As the employer, you can contribute up to 25% of your net income, which increases your contribution limit to $66,000 if you are under 50, or $73,500 if you are 50 or older.

- Roth Contributions: You can also make Roth contributions, which are made with after-tax dollars and are tax-free in retirement.

SEP IRA Contribution Structure

- Employer-Only Contributions: Contributions to a SEP IRA are made only by the employer, and these contributions can be up to 25% of compensation. The maximum contribution for 2023 is $66,000.

- No Catch-Up Contributions: Unlike the Solo 401(k), the SEP IRA does not allow catch-up contributions for individuals age 50 or older.

Contribution Limits for Solo 401(k) vs. SEP IRA

To make an informed decision about which retirement plan to use, you need to know the contribution limits for both the Solo 401(k) and the SEP IRA. Although both plans have high contribution limits, they differ in their limits.

Solo 401(k) Contribution Limits

- Employee Contributions: For 2023, you can contribute a maximum of $22,500 as an employee, and an additional $7,500 as a catch-up contribution if you are 50 years of age or older, increasing the total employee contribution to $30,000.

- Employer Contributions: You can also contribute a maximum of 25% of your net income as the employer. The total of both employee and employer contributions cannot exceed $66,000 (or $73,500 with catch-up contributions for those 50 and older).

- Total Contribution: The maximum contribution to a Solo 401(k) plan is as high as $66,000 (or $73,500 for those 50 and older).

SEP IRA Contribution Limits

- Employer Contributions: Contributions are made only by the employer, and you can contribute up to 25% of your compensation. The maximum contribution for 2023 is $66,000.

- No Catch-Up Contributions: Unlike the Solo 401(k), the SEP IRA does not allow catch-up contributions for individuals age 50 or older, which limits the contribution potential for individuals close to retirement.

How Solo 401(k)s Work

The Solo 401(k) plan is specifically designed for self-employed individuals and business owners with no employees, except for a spouse. The Solo 401(k) plan allows for both employee and employer contributions, making it one of the most flexible and powerful retirement plans available to business owners.

Eligibility and Setup

A Solo 401(k) plan is available to sole proprietors, independent contractors, and business owners with no employees (except for a spouse). To set up a Solo 401(k) plan, you will need to decide whether you want a traditional or Roth Solo 401(k) plan and choose a financial institution to administer your plan.

Setting up a Solo 401(k) plan is more complex than other retirement plans, but it is still relatively easy. Your plan administrator will assist you in setting up the necessary paperwork and help you comply with IRS regulations.

Contributions and Tax Advantages

- Employee Contributions: You can contribute up to $22,500 in 2023 as an employee, with catch-up contributions allowed if you are 50 or older.

- Employer Contributions: You can also contribute up to 25% of your net income as the employer. The total contributions (employee + employer) can be up to $66,000 (or $73,500 with catch-up contributions for those 50 or older).

- Tax Advantages: Contributions to a Solo 401(k) plan are made with pre-tax dollars, which reduces your taxable income for the year. If you choose a Roth Solo 401(k) plan, you pay taxes on contributions, but withdrawals are tax-free in retirement. If tax-free retirement income is your goal, a gold roth IRA may be worth exploring.

Benefits of a Solo 401(k) Plan

- Higher Contribution Limits: With both employee and employer contributions, the Solo 401(k) plan has the highest contribution limits of any retirement plan available to the self-employed.

- Flexibility: You can choose to make Roth contributions for tax-free growth and retirement income.

- Loan Feature: The Solo 401(k) plan also allows you to take a loan against your plan (up to $50,000 or 50% of the plan’s value), which is not allowed with a SEP IRA.

How SEP IRAs Work

The SEP IRA is a retirement plan designed for self-employed individuals, freelancers, and small business owners seeking a low-maintenance option. The SEP IRA allows only employer contributions, which makes it a great option for business owners who want to contribute to their own retirement without the hassle of administering a Solo 401(k).

Eligibility and Setup

- The SEP IRA is available to any business, whether you are self-employed, a freelancer, or a small business owner. There are no requirements for having employees, but if you do, you are required to contribute on their behalf as well.

- Setting up a SEP IRA is much easier than setting up a Solo 401(k).

Contributions and Tax Advantages

- Employer Contributions: Employers are allowed to contribute up to 25% of an employee’s or their own compensation, up to a maximum of $66,000 in 2023.

- Tax Advantages: Similar to the Solo 401(k) plan, the SEP IRA has a tax-deferred feature, which means that you, the contributor, will not be required to pay taxes on your contributions until you retire and withdraw the funds. However, unlike the Solo 401(k) plan, the SEP IRA does not have a Roth contribution option for tax-free withdrawals. If you already have IRA savings and want to diversify, you may be able to convert ira to gold through an eligible transfer or rollover process.

Advantages of SEP IRA

- Ease of Administration: The SEP IRA is very easy to administer, making it the best choice for small business owners or sole proprietors who are looking for a simple retirement plan solution with minimal paperwork.

- High Contribution Limits: Although the SEP IRA is easy to administer, it still has high contribution limits of up to $66,000 in 2023, making it a great choice for business owners who are looking to save for retirement.

Conclusion

The Solo 401(k) and SEP IRA are both excellent options for self-employed individuals and small business owners to save for retirement. If you are looking to contribute more to your retirement savings and have the flexibility to do so, then the Solo 401(k) may be the better option for you. But if you are looking for a retirement plan that is easier to administer and requires less paperwork, then the SEP IRA may be a great option for you to build your retirement savings.

At Opulent Gold Group, we recognize the value of making informed decisions regarding your financial future. Whether you are a small business owner or a freelancer, selecting the right retirement plan is one way to ensure that you have financial security in retirement. If you’re also thinking about diversifying beyond traditional assets, explore how a gold IRA could fit into a long-term retirement strategy.

FAQ

What is the main difference between a Solo 401(k) and a SEP IRA?

The Solo 401(k) allows contributions as both an employee and an employer, while the SEP IRA only allows employer contributions, with lower contribution limits.

Can I contribute to both a Solo 401(k) and a SEP IRA?

No, you can only contribute to one plan in a given year.

How much can I contribute to a Solo 401(k) in 2023?

You can contribute up to $22,500 as an employee, plus an additional $7,500 if you’re 50 or older. Employer contributions can be up to 25% of your net income, with a total of $66,000 ($73,500 with catch-up).