When it comes to securing your financial future, retirement planning is one of the most important steps you can take. Two of the most popular retirement options—IRAs and 401(k)s—each offer unique advantages, but choosing the right one for your needs can be a challenge. From tax benefits and contribution limits to investment flexibility, understanding the differences between these two plans is key to making the best choice for your retirement goals. In this blog post, we’ll explore the key differences between IRAs and 401(k)s, break down the types of each, and help you determine which plan is the best fit for your financial future. At the end of the day, Opulent Gold Group is here to guide you toward making the right retirement decisions for a secure future.

What is an IRA? Understanding Individual Retirement Accounts

Individual Retirement Accounts (IRAs) are investment accounts that enable individuals to save for retirement while enjoying some tax benefits. There are various types of IRAs, each with its own set of tax benefits and portability rules.

Types of IRAs

- Traditional IRA: With a Traditional IRA, you can deduct your contributions from taxes, and the money grows tax-deferred. You will pay taxes when you withdraw the money in retirement.

- Roth IRA: With a Gold Roth IRA, you pay taxes on the contributions you make, and the investment grows tax-free. Withdrawals in retirement, including earnings on your contributions, are also tax-free.

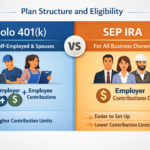

- SEP IRA (Simplified Employee Pension): This type of IRA is suited for self-employed individuals and small business owners. It has higher contribution limits than a Traditional IRA.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): This is a type of IRA commonly used by small business owners. It allows both employee and employer contributions, but is easier to administer than other types of IRAs.

Advantages of an IRA

- Tax Benefits: Depending on the type of IRA, you may get tax deductions or tax-free growth, making it a valuable tool for retirement planning.

- Investment Flexibility: A Gold IRA offers a unique investment opportunity, allowing you to invest in physical gold and other precious metals, providing a hedge against inflation and market volatility.

Disadvantages of an IRA

- Contribution Limits: The contribution limits for IRAs are lower compared to 401(k) plans, which might limit how much you can save each year.

- Early Withdrawal Penalties: Withdrawing funds from an IRA before age 59½ typically results in penalties, although there are exceptions.

What is a 401(k)? Exploring Employer-Sponsored Retirement Plans

A 401(k) is an employer-sponsored retirement plan that allows employees to save a portion of their salary for retirement. These plans often include additional benefits, such as employer-matching contributions. If you’re interested in diversifying your retirement savings, consider converting your 401k to gold for added protection against market fluctuations.

Types of 401(k) Plans

- Traditional 401(k): Employees contribute pre-tax dollars, and the contributions grow tax-deferred until retirement, at which point withdrawals are taxed as ordinary income.

- Roth 401(k): With a Roth 401(k), employees contribute after-tax dollars, and qualified withdrawals in retirement are tax-free.

- Solo 401(k): A plan designed for self-employed individuals and small business owners, allowing them to contribute both as an employer and an employee.

- SIMPLE 401(k): Similar to a SIMPLE IRA, this plan is designed for small businesses and has lower administrative costs.

Advantages of a 401(k)

- Higher Contribution Limits: The contribution limits for 401(k) plans are significantly higher than those for IRAs, allowing you to save more for retirement.

- Employer Matching Contributions: Many employers match a percentage of your contributions, essentially providing “free money” for your retirement.

Disadvantages of a 401(k)

- Limited Investment Options: 401(k) plans typically offer a limited selection of employer-selected investments that may not align with your personal investment preferences.

- Potential High Fees: Some 401(k) plans come with high administrative or fund management fees, which can reduce your overall returns.

Key Differences Between the 401(k) and an IRA

Now that we’ve covered the basics, let’s dive into the key differences between these two popular retirement plans. Understanding these differences will help you decide which is best for your retirement strategy. If you’re looking to further diversify, you may want to explore how to convert ira to gold for added stability in your portfolio.

Contribution Limits: IRA vs. 401(k)

One of the biggest differences between an IRA and a 401(k) is the contribution limit. For 2026, the contribution limit for an IRA is $6,000 ($7,000 if you’re 50 or older). In comparison, the contribution limit for a 401(k) plan is much higher, at $22,500 ($30,000 if you’re 50 or older). This means that if you’re looking to save as much as possible, a 401(k) might be the better option.

Tax Advantages and Benefits

- Traditional IRA vs. Traditional 401(k): Both plans allow you to contribute pre-tax dollars, reducing your taxable income for the year. However, when you withdraw the funds in retirement, you’ll pay taxes on the money you take out.

- Roth IRA vs. Roth 401(k): Both of these accounts allow you to contribute after-tax dollars, but the biggest difference is that Roth 401(k)s may be subject to Required Minimum Distributions (RMDs) in retirement. At the same time, Roth IRAs do not have RMDs during the account holder’s lifetime.

Employer Contributions: IRA vs. 401(k)

With a 401(k), many employers offer a matching contribution, which can be a huge advantage. For example, an employer may match your contribution up to a certain percentage, providing you with free money for your retirement. However, there are no employer contributions with an IRA.

Withdrawal Rules and Penalties

- IRAs: You can generally start withdrawing from an IRA without penalty at age 59½. Early withdrawals may be subject to a 10% penalty plus income tax, though there are exceptions.

- 401(k): With a 401(k), the withdrawal rules are similar, but 401(k) plans also require RMDs beginning at age 73, even if you don’t need the funds.

Is It Better to Have a 401(k) or an IRA? Pros and Cons

Choosing between an IRA and a 401(k) depends on your individual financial situation and retirement goals. Let’s take a closer look at when each option might be more beneficial.

When a 401(k) Might Be the Better Choice

- Employer Matching Contributions: If your employer offers a match, contributing to your 401(k) is free money for your retirement.

- Higher Contribution Limits: If you want to save as much as possible for retirement, the higher contribution limits of a 401(k) make it an attractive option.

- Automatic Contributions: 401(k) contributions are automatically deducted from your paycheck, making saving for retirement easy and consistent.

When an IRA Might Be the Better Choice

- Investment Flexibility: With an IRA, you have far more investment options compared to a 401(k). This flexibility can be beneficial if you prefer a diverse portfolio.

- Lower Fees: IRAs often have lower management fees than 401(k) plans, which can help you keep more of your investment returns.

- Ideal for Self-Employed Individuals: If you’re self-employed, an IRA offers an easy and affordable retirement saving option without the administrative burdens of a 401(k).

Can You Have Both an IRA and a 401(k)?

Yes, it’s possible to contribute to both an IRA and a 401(k) in the same year. However, keep in mind that there are contribution limits for each account type. Contributing to both plans allows you to maximize your retirement savings potential, but you’ll need to consider whether it fits within your overall financial plan.

How to Choose the Right Plan for Your Retirement

Now that you have a clearer picture of the differences between a 401(k) and an IRA, how do you decide which one is right for you?

Assessing Your Financial Goals

Consider your long-term retirement goals and how much you plan to contribute each year. If you’re aiming for a larger retirement fund, a 401(k) may be the best option given its higher contribution limits.

Considering Your Employment Status

Are you employed with a company that offers a 401(k) match? If so, taking full advantage of the employer match is generally a smart move. If you’re self-employed, an IRA may be the more flexible option.

Talking to a Financial Advisor

A financial advisor can help you assess your situation and guide you in choosing the right retirement plan for your needs. They can also help you strategize how to use both an IRA and a 401(k) effectively if you choose to contribute to both.

Conclusion

Choosing between a 401(k) and an IRA ultimately comes down to your personal retirement goals and financial situation. If you’re looking for higher contribution limits and the potential for employer matching, a 401(k) may be the better option. However, if you value investment flexibility and lower fees, an IRA could be a great choice. No matter which option you choose, planning is crucial. At Opulent Gold Group, we are dedicated to helping you make the best financial decisions to build lasting wealth. Reach out to us today and let us help you plan for a secure and prosperous retirement.

FAQ

What’s the main difference between an IRA and a 401(k)?

The main difference is that a 401(k) is employer-sponsored, while an IRA is an individual account. 401(k)s offer higher contribution limits, while IRAs provide more investment flexibility.

Can I contribute to both an IRA and a 401(k)?

Yes, you can contribute to both, but there are separate contribution limits for each.

Which plan has higher contribution limits?

A 401(k) has higher contribution limits than an IRA. For 2026, you can contribute up to $22,500 to a 401(k) ($30,000 if over 50), compared to $6,000 for an IRA ($7,000 if over 50).